- Energized

- Posts

- ⚡The Trade War is On

⚡The Trade War is On

Crude, nat gas and dollar are higher, equities tanking.

February 3, 2025

PRESENTED BY: EKT INTERACTIVE ENERGY TRAINING

Morning, and welcome to February. Energized is now on the Beehiiv newsletter platform, which won’t matter much to you but I’m excited about it.

The trade war is on with 25% tariffs on Canada and Mexico in effect. Oil got a little break (10% tariff) but not a full exemption. China also got an additional 10%.

Equities are down big as I write this and the dollar is ripping. The market has been shrugging of the uncertainties that a trade war will bring to our own economy, but it was only a question what the details might look like - bad or really bad.

Post FOMC, it’s a busy week of various Fed governors speaking. Lots to talk about but we’ll see what they say.

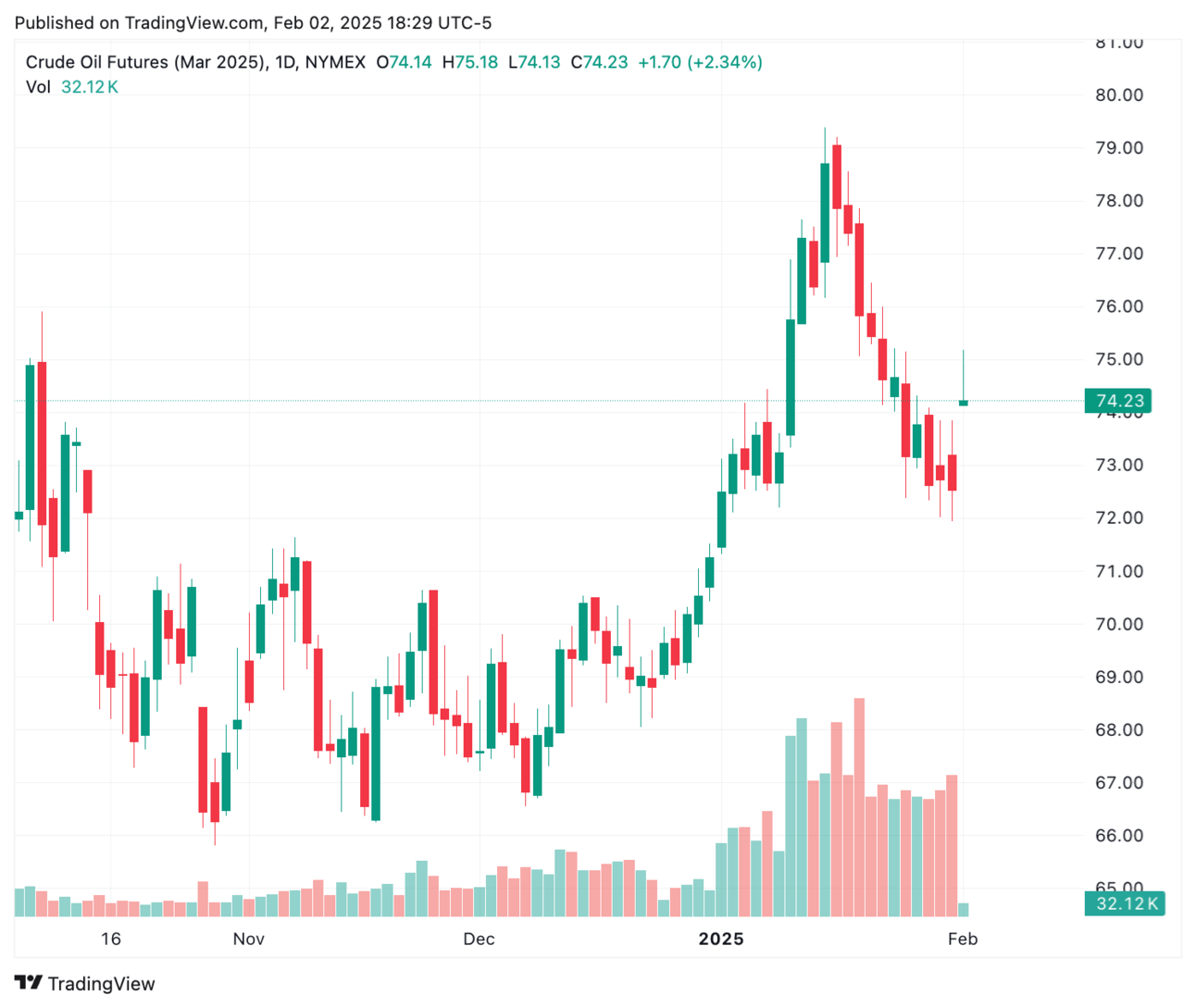

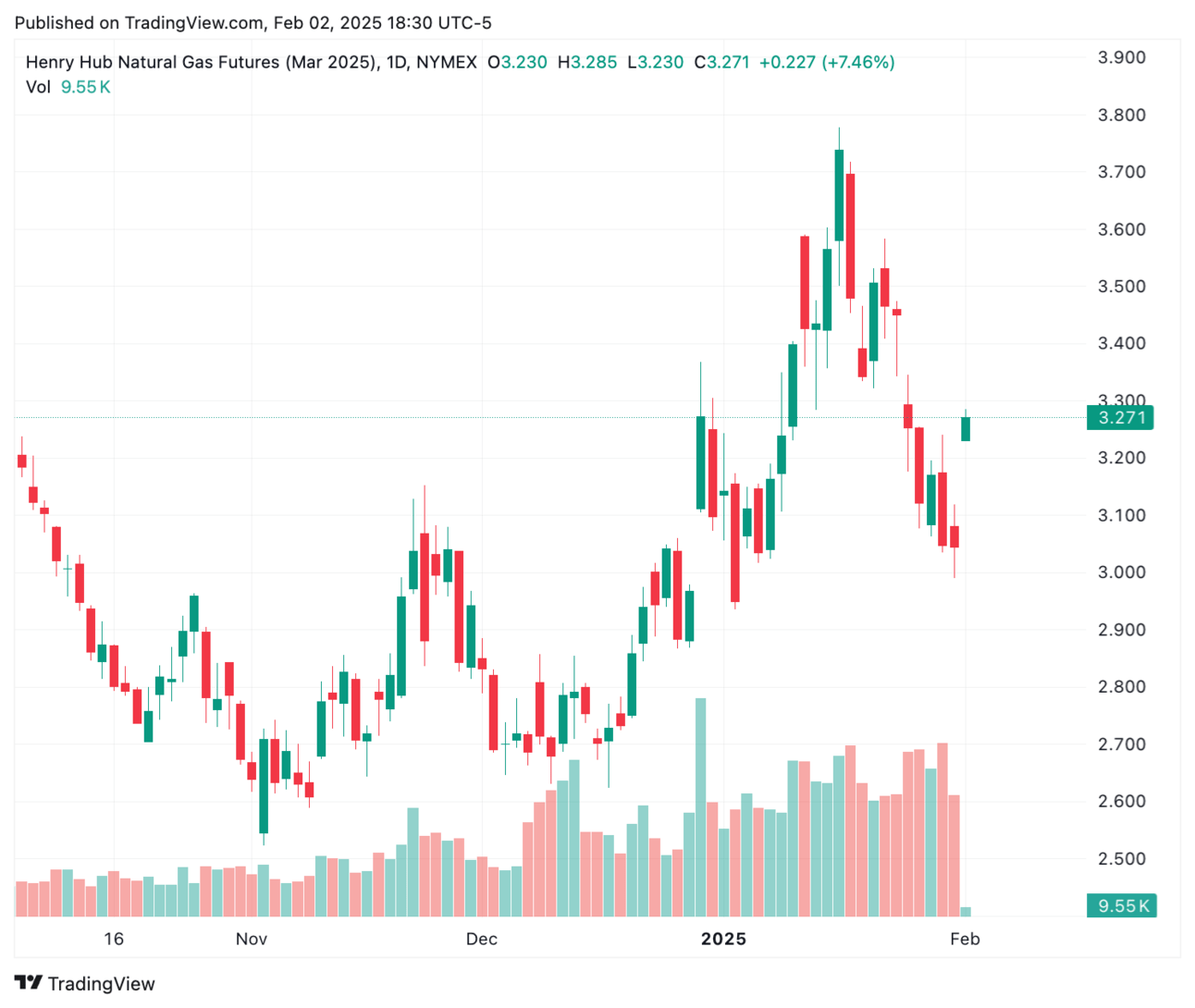

WTI is up 2.5% and had traded as high as $75. Nat gas is up 8.5%. The closing prices below don’t mean much, except as a reminder that for two days the market was unchanged as it awaited the final word on tariffs.

What's in this issue:

Energy Market Recap

Trade War is On

The Market You Have

Headlines

| Crude Oil (Mar) | $73.53 | -0.20 | -0.27% |

| Natural Gas (Mar) | $3.044 | -0.003 | -0.01% |

| Copper (Mar) | $4.2790 | -0.0285 | -0.66% |

| S&P 500 | 6,040.53 | -30.64 | -0.50% |

| Dollar Index (DXY) | 108.22 | +0.35 | +0.32% |

ENERGY MARKETS

🛢️Oil prices took the last couple of trading sessions off last week as we all awaited clarity on tariffs. Prices ended lower by 2.85% on the week.

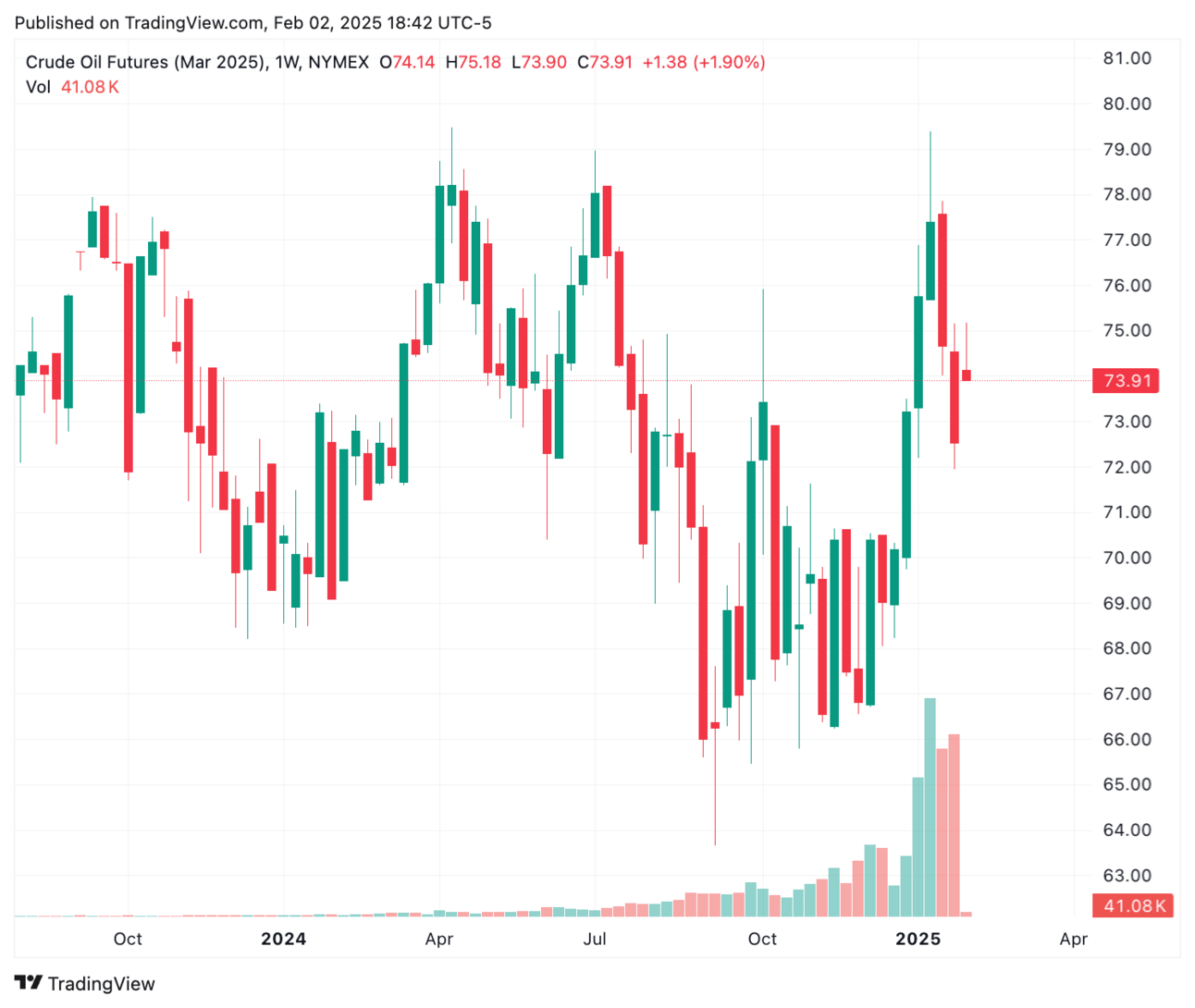

I think it’s worth taking a look at this weekly chart below, just to refresh a longer term perspective. Serious resistance around $79.00-79.50 basis March, not just from the last move higher, but from two previous moves as well.

WTI Spreads

Mar/Apr: +0.55

Mar/Dec: +4.77

Dec5/Dec6: +2.64

🔥Natural gas ended last week lower by almost 12% and unraveled an incredible 25% from the recent highs recorded at the peak of the recent arctic blast.

The expiration of the February contract took winter demand with it, however the uncertainty in the market has sent prices higher overnight.

Trade War is On

The capitulation of Colombia may have given the impression that the tariff game was going to be completely one-sided, and that played into the vision Trump has sold. That was always unlikely to be the case and now we’re about to find out the cards other players at the table have.

Lopsided? sure, but not one-sided. The WSJ has called this “The Dumbest Trade War In History”, the FT calls it “Absurd". Agree?

I’ve been covering our reliance on Canadian oil since the threat of tariffs began, but here’s a great deep dive Great piece by Ed Conway the subject.

What Will Retaliation Look Like?

There will be retaliatory moves from all of the countries involved. It’s just a matter of what they look like, and what they leave out. The expectation is for more targeted responses on industries that have loud voices in Washington.

We’ve been here before.

“Retaliation worked in 2018, when Mexico responded to U.S. tariffs on steel with tariffs of its own that included steel, pork, cheese, apples and bourbon. The U.S. eventually backed down.“

THE MARKET YOU HAVE

When it comes to the markets themselves, it’s impossible to predict what’s next. As Goldman Sachs passed on to their clients and was quoted in the WSJ:

“the state of negotiations and potential for a quick reversal makes this more uncertain.”

It’s headline to headline, tweet to tweet. In general, markets hate this level of uncertainty. But the danger of reversals is real.

HEADLINES

“Rubio delivered a message from Trump that China's presence - through a Hong-Kong based company operating two ports near the canal's entrances - was a threat to the waterway and a violation of the U.S.-Panama treaty”

+Rubio tells Panama to end China's influence of canal or face US action - Reuters

“Vitol, which trades about 7 per cent of the world’s oil supply every day, expects global demand to peak at almost 110mn barrels per day at the end of this decade, and then retreat to current levels of about 105mn b/d in 2040.”

+Oil demand to remain at current levels until at least 2040, Vitol says - FT

“But total coal-fired power generation hit new highs in India last year, so lower imports mean that higher volumes of domestic coal were burned for power instead, and that's bad news for emissions levels.”

+India's lower coal imports mean bad news for power emissions - Reuters

ECONOMIC CALENDAR

Monday - PMI, ISM

Tuesday - Job Openings, Factory Orders, Fed Atlanta & San Fran speak,

Wednesday - ADP Employment, Crude Oil Storage Report

Thursday - Natural Gas Storage Report, Jobless Claims, Fed speakers

Friday - Employment