- Energized

- Posts

- ⚡WTI Catches a Bid

⚡WTI Catches a Bid

Plus, steel and aluminum join the tariff party.

February 11, 2025

PRESENTED BY: ENERGY 101

I’m sitting on my couch trying to get this issue done before I pass out. I don’t really like coming back from a trip feeling rested. I prefer to return feeling like I’ve been well worked over, and a solid pummeling in the surf at an undisclosed Central American location did the trick.

Still managed to get Energized out each day though! Ironically, today, back at home, is the toughest.

Same routine here. Daily headlines on sanctions and tariffs, with steel and aluminum being the latest to join the party.

Eyes on Wednesday’s CPI number as expectations of a rate cut before June have declined and crude inventory data to see if last week’s large build was a one-off.

What's in this issue:

Energy Market Recap

Recommended Interview: John Kemp

Copper Moves

Headlines

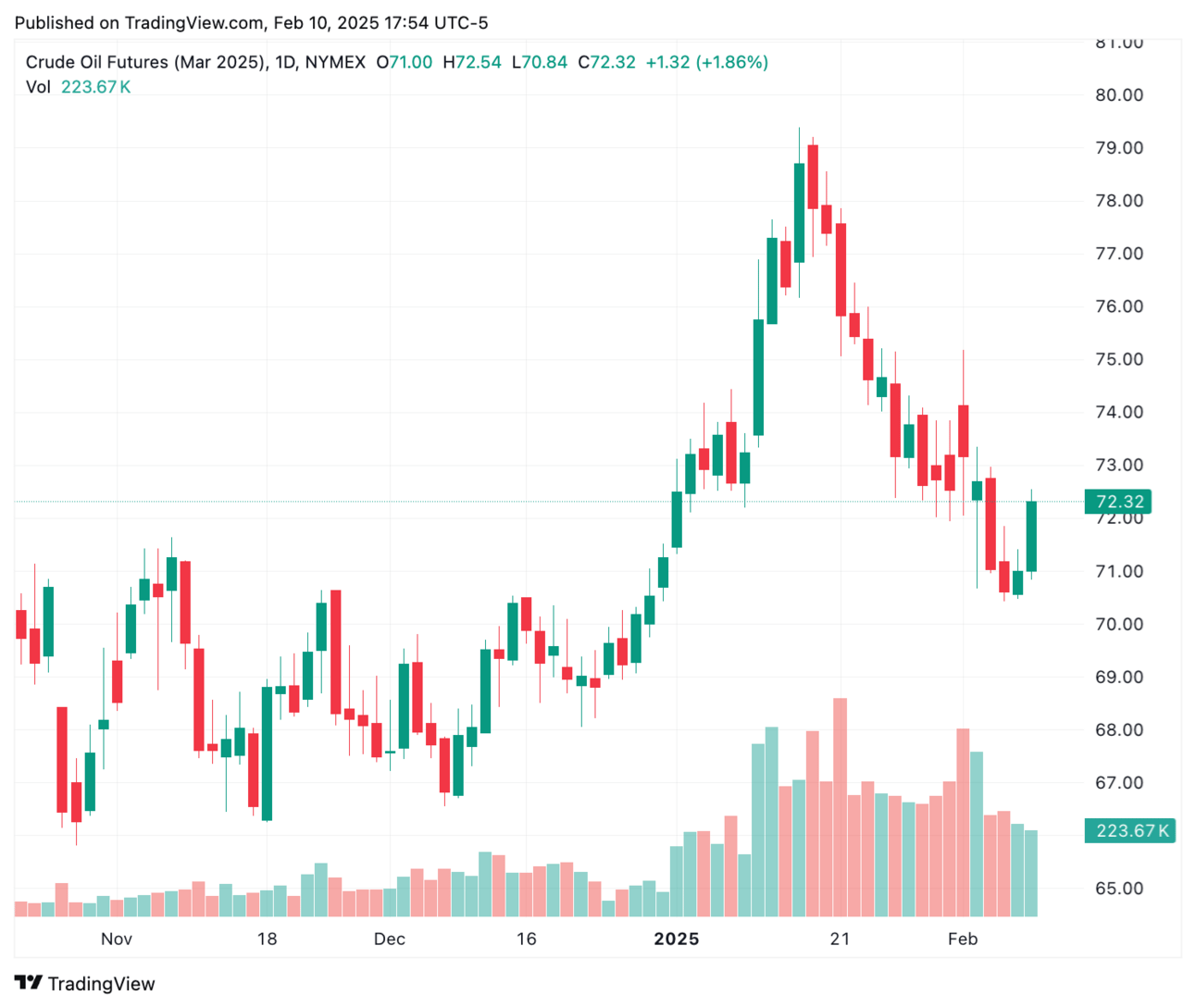

| Crude Oil (Mar) | $72.32 | +1.32 | +1.86% |

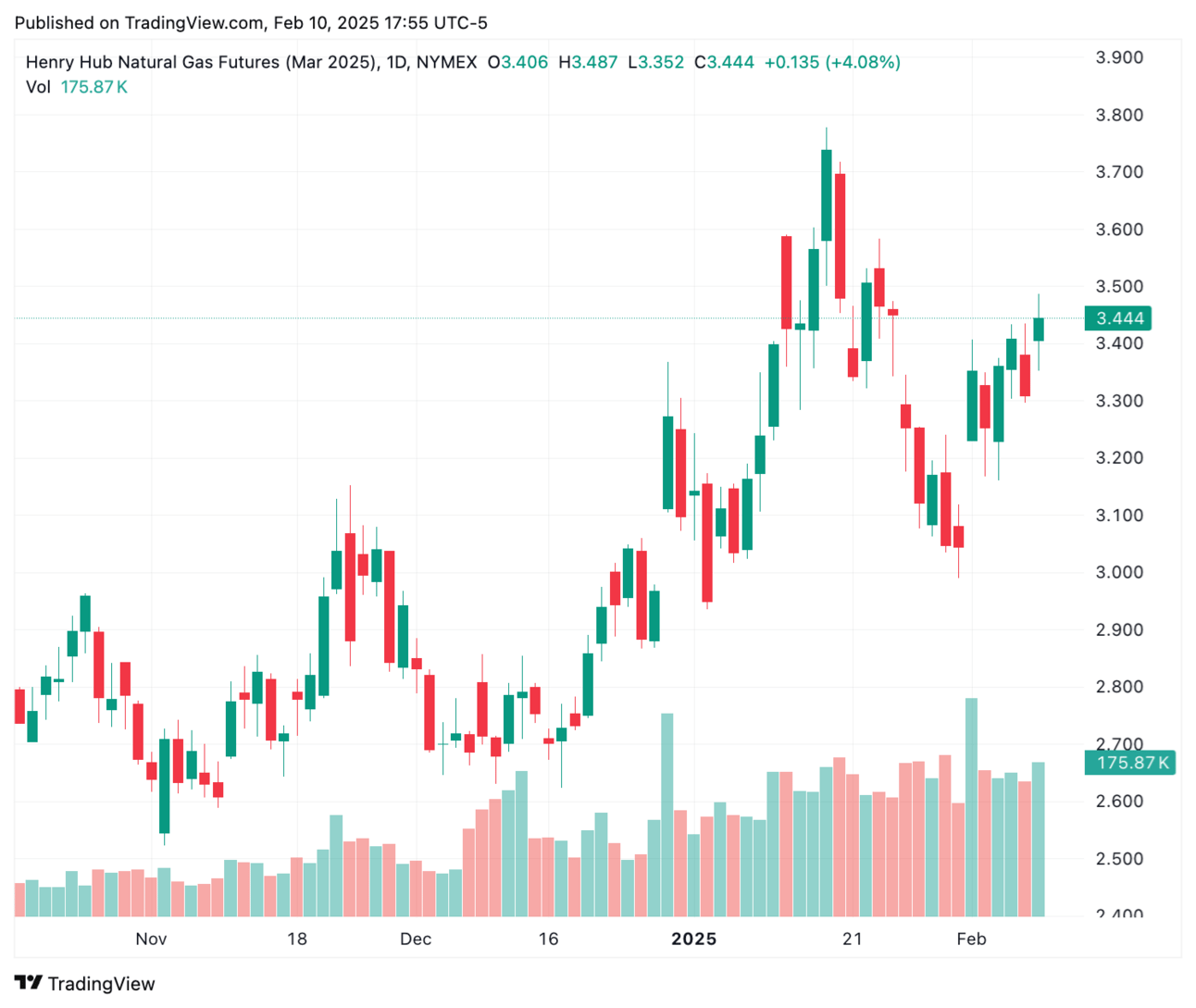

| Natural Gas (Mar) | $3.444 | +0.135 | +4.08% |

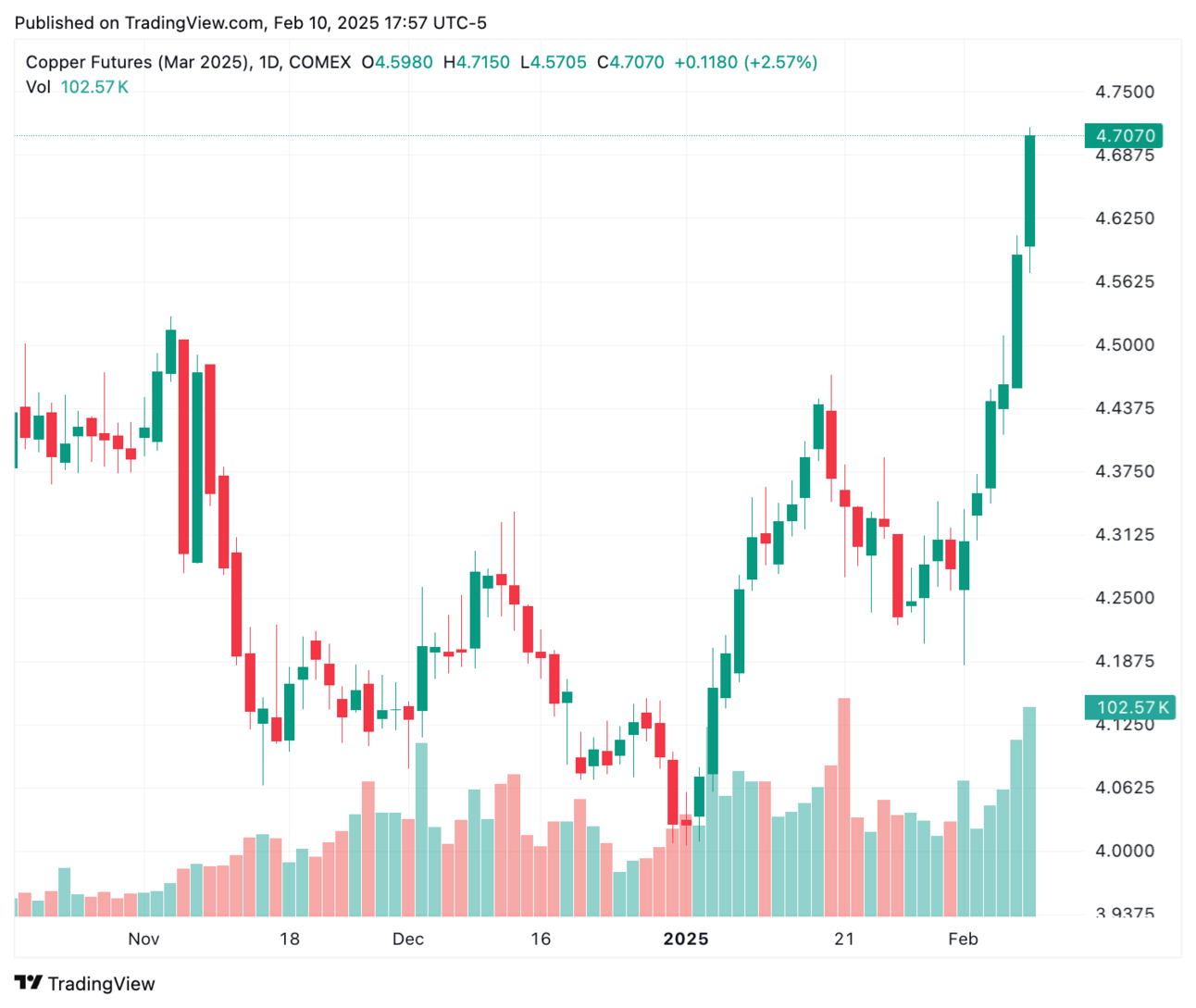

| Copper (Mar) | $4.7070 | +0.1180 | +2.57% |

| S&P 500 | 6,066.44 | +40.45 | +0.67% |

| Dollar Index (DX) | 108.19 | +0.16 | +0.15% |

ENERGY MARKETS

🛢️Oil prices moved higher by almost 2%, although hard to call this a reversal just yet. Volume of these last few sessions has been low.

Upside risks include more details on sanctions on Iran, or new ones on Venezuela. Downside risks include a global economic slowdown.

As analyst John Kemp highlights in the interview linked below, it’s hard to see OPEC coming to the rescue before prices hit $90 or more.

OPEC is quick to support falling prices and slow to put a lid on rising ones.

WTI Spreads

Mar/Apr: +0.31

Mar/Dec: +3.72

Dec5/Dec6: +2.71

🔥Natural gas prices were higher by 4% as the cold weather + declining inventories narrative continues to hold for the middle of the month.

PRESENTED BY ENERGY 101

How the Energy Industry Works

“ Although I’m not an engineer, the course gave me many useful tools to understand the technicalities of the industry. Now I can communicate easily with my contacts in the energy sector.

RECOMMENDED LISTEN

Energy market analyst John Kemp summarizes everything from global oil balances, US natural gas and LNG, and the European power predicament in this excellent interview.

China Demand

One of the key points on oil he brings up is the balance between the potential for sanctions to remove barrels from the market versus the negative macro influence of a trade war.

Before Trump took office, the main question facing oil demand was whether China’s economy would recover in 2025 (the other being the forecasted supply overhang).

That recovery will be even harder in the current environment, and is clearly offsetting the upside risks to oil prices at the moment.

Russia Exports

I highlighted an article a couple weeks back that, among EU politicians, talk of bringing Russian pipelines back online is becoming less taboo.

Kemp highlights the current predicament Europe finds itself in with high gas and electricity prices, and how it’s hard to imagine any negotiated end to the war in Ukraine without some lifting of sanctions on Russian oil and gas.

Fascinating turn of events if that comes true.

US Nat Gas

Kemp highlights that, despite the recent price rise, US gas is still super cheap - probably too cheap to spur new production.

Combined with the incentive to run gas power production at full capacity, this spells continued tightening and price rises in US gas.

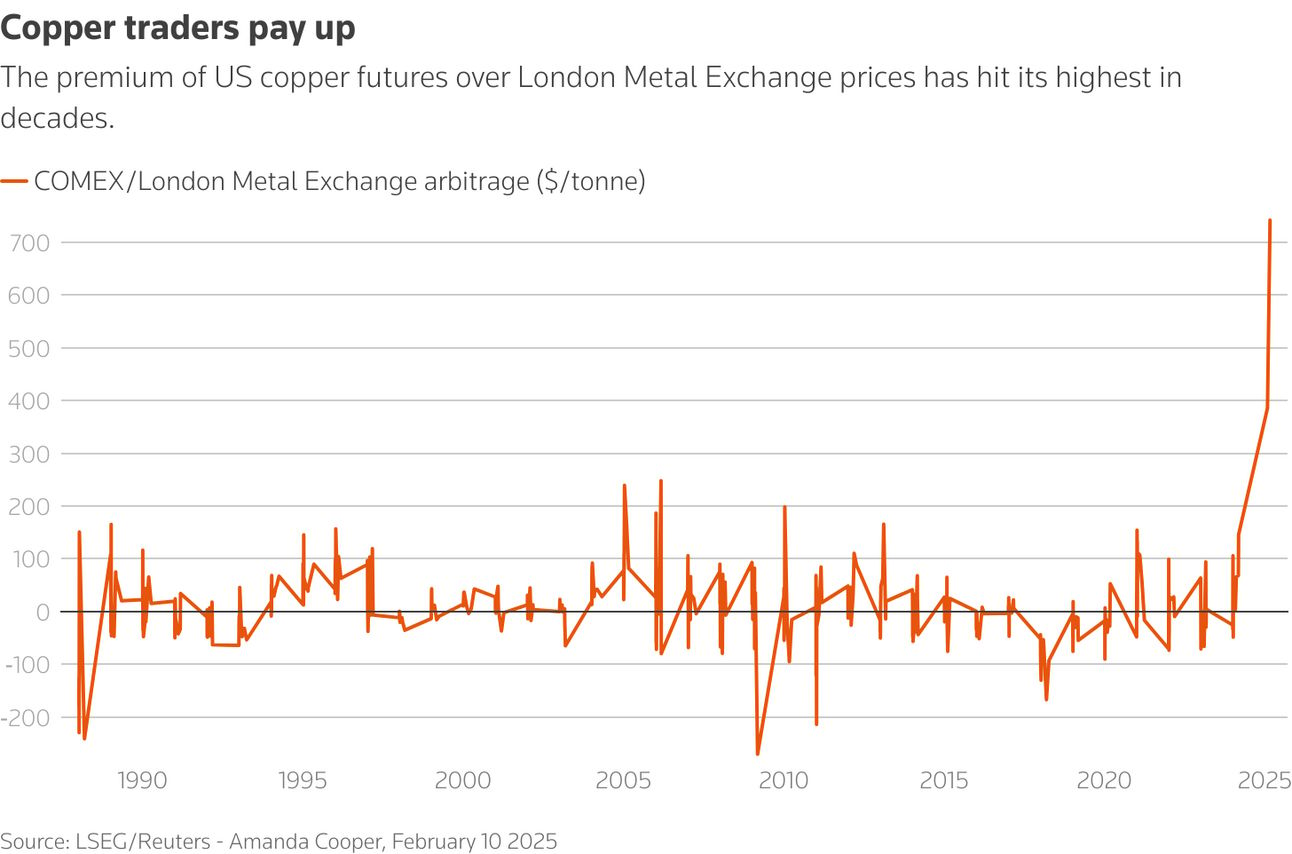

COPPER MOVES

I just wanted to include this chart of copper considering steel and aluminum are getting the same treatment.

“It’s 25%, without exceptions or exemptions. And that’s all countries, no matter where it comes from.”

+Trump Imposes Global 25% Steel, Aluminum Tariffs - WSJ

However, don’t mistake this move as Dr. Copper diagnosing a robust global economy.

As Reuters points out, the price rise is just happening in the US:

“right now, this has less to do with optimism over global growth and more with where traders are moving metal to stave off potential tariff risks.”

Much like moves in the gold market we highlighted recently, the spread between LME and COMEX futures prices shows this is more to do with where commodities are located than macro supply/demand dynamics.

Source: Reuters

HEADLINES

“We used to have competitors,” Walz said. “They’re gone.”

+Behind the Oil Industry’s Biggest Divorce: Chevron Versus California - WSJ

“Elliott could push BP on five fronts, according to Jefferies International Ltd. analyst Giacomo Romeo. These include a refocus on traditional oil and gas, leaving low-carbon activities, monetizing assets that can attract higher multiples such as infrastructure and retail components, maximizing free cash flow generation by reducing capital spending, and increasing the pace of divestments.”

+BP Shares Jump After Activist Investor Elliott Builds Stake - Bloomberg

"While Energy Transfer did not provide project costs or returns, we view the announcement favorably as a concrete example of how midstream players can directly participate in the AI/datacenter thematic,"

+Energy Transfer signs natural gas supply agreement with CloudBurst - Reuters

"Panic has finally shown up”

+Coffee futures in New York jump 6% to new record amid 'panic buying' - Reuters

ECONOMIC CALENDAR

Monday -

Tuesday -

Wednesday - CPI, Crude Oil Storage Report

Thursday - Natural Gas Storage Report, Jobless Claims, PPI

Friday - Retail Sales